Should I Invest All at Once or Systematically Over Time?

Should I Invest All at Once or Systematically Over Time?

Aug 3, 2021 / By Craig L. Israelsen, PhD

New investors or those moving from the sidelines back into equity investments are faced with two entry strategies: lump sum or monthly? This 40-year performance analysis points the way.

A classic investing question is “What should I invest in?” Nearly as important is the sequel question “How should I invest—all at once or periodically?” For investors who have a choice between a lump-sum investment or a periodic investment (say, monthly), this second question is a big deal.

Another group of investors facing this second question are those who exited their equity-based portfolios at some point in the past and are now considering moving from the sidelines back into equity investments. These folks are faced with two re-entry strategies: (1) jump back in all at once with a lump sum or (2) ease back in by degree making systematic investments each year or each month.

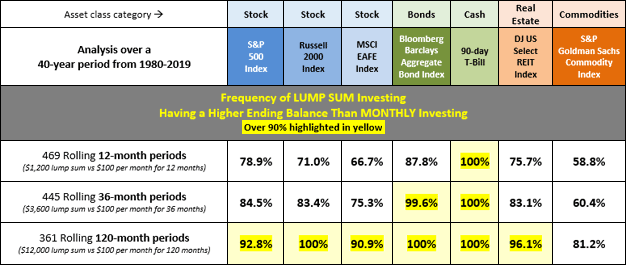

Shown below are seven core asset classes (indexes) that represent the primary ingredients in most portfolios. Each asset class was studied to determine how often a lump-sum investment outperformed a monthly investment over a 40-year period from January 1980 through December 2019. “Outperformance” was determined by ending dollar balance over 469 rolling 12-month periods, 445 rolling 36-month periods and 361 rolling 12-month periods.

For example, consider the S&P 500 Index (large cap U.S. stock). A lump-sum investment of $1,200 had a higher ending balance than a $100 per month investment in 78.9% of the 469 rolling 12-month periods. That means that a monthly investment outperformed roughly 21% of the time. As you might guess, monthly investing tended to be better than lump sum during bear equity markets.

When we examine rolling 36-month holding periods, lump-sum investing into the S&P 500 Index was superior to monthly investing 84.5% of the time. Over rolling 120-month periods (10 years) lump sum outperformed monthly investing nearly 93% of the time.

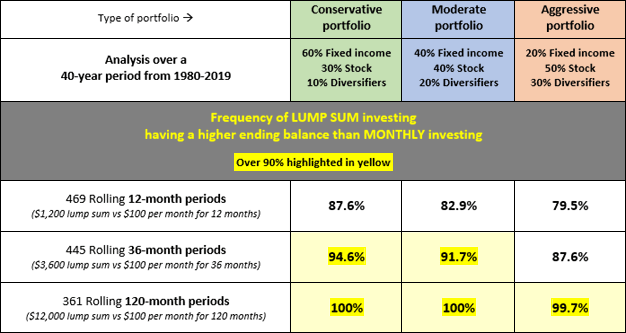

Table 1: Lump Sum vs. Monthly Investing40-year period from 1980–2019

Source: Craig Israelsen

If investing in small cap U.S. stock (Russell 2000 Index), lump sum was superior to monthly investing 71% of the time over rolling 1-year periods, 83.4% over rolling 3-year periods, and 100% of the time over rolling 10-year periods.

Investing in bonds and cash via a lump-sum investment is nearly always better than doing so via a monthly investment—regardless of time frame. Commodities, on the other hand, is an asset class in which systematic investing often makes sense. Over rolling 12-month periods, a lump-sum investment into the Goldman Sachs Commodity Index outperformed a monthly investment just under 59% of the time. Over rolling 36-month periods, lump sum outperformed monthly investing 60.4% of the time. For longer-term investors, lump-sum investing into commodities is clearly superior to monthly investing based on having a higher ending balance 81% of the time. However, the other six asset classes had a higher lump-sum ending balance over 90% of the time over rolling 120-month periods.

Blending indexes together into diversified multi-asset portfolios

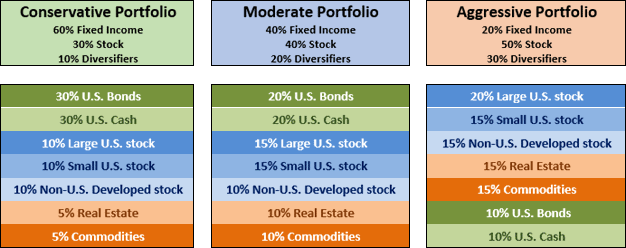

The seven indexes in Table 1 represent components in a diversified investment portfolio. Think of them as ingredients in salsa. Shown below are three portfolios that were studied over the same 40-year period: a conservative portfolio, a moderate risk portfolio and an aggressive portfolio.

The conservative portfolio (60/30/10) has an overall asset allocation of 60% fixed income, 30% stock and 10% diversifiers. Specifically, it has a 30% allocation to bonds, 30% to cash, 10% each to large U.S. stock, small U.S. stock, and non-U.S. stock and 5% each to real estate and commodities.

The moderate portfolio (40/40/20) decreases the bond and cash allocation to 20%, lifts the U.S. stock allocations to 15% each and allocates 10% to both real estate and commodities. The aggressive portfolio (20/50/30) allocates 20% to large U.S. stock, 15% each to small U.S. stock and non-U.S. stock, 15% each to real estate and commodities and 10% each to bonds and cash.

Unless otherwise stated, the multi-asset portfolios were rebalanced monthly in the rolling-period performance analysis (rebalancing maintains the specified allocations from month to month).

Table 2: Three Diversified, Multi-Index PortfoliosConservative, Moderate, Aggressive

Source: Craig Israelsen

As shown below in Table 3, when investing in a diversified portfolio (rather than single asset classes) there is an 80% or higher chance that a lump-sum investment will finish with a higher balance compared to equal monthly investments after 12 months (based on historical results). For investors with a 36-month horizon, a lump-sum investment produced a higher ending balance at least 87% of the time (and 94% of the time for a conservative portfolio). For investors who commit to a 10-year holding period, it is clear that a lump sum investment produces the best results. All that said, it assumes the investor can weather the natural ups and downs of their portfolio balance along the way.

In general, the more conservative the portfolio, the safer it is to wade back into the “market” via a lump-sum investment.

Table 3: Lump Sum vs. Monthly Investing40-year period from 1980–2019